Constant Marginal Costs Occur When Each Individual Unit Costs

Figure 1 illustrates the idea of economies of scale showing. The marginal cost curve is generally upward-sloping because diminishing marginal returns implies that additional units are more costly to produce.

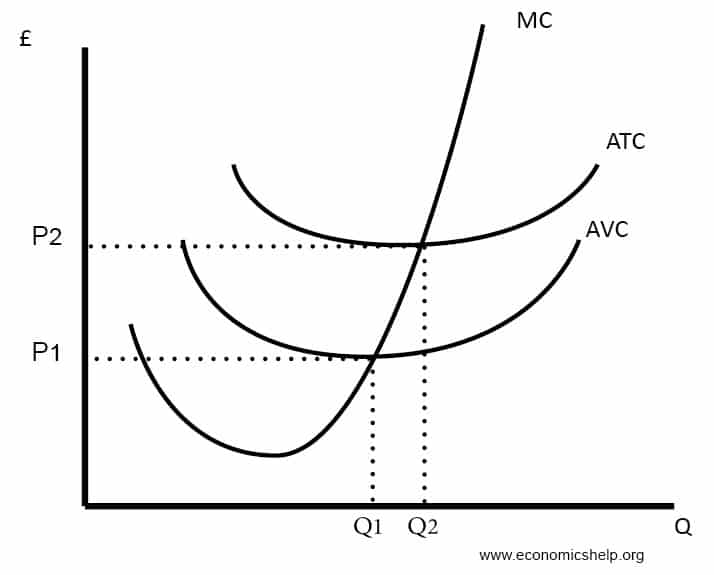

Costs Of Production Maple Help

3 The costs associated with variable inputs are ____ and the costs associated with ___ inputs are ____.

. More formally marginal cost is the cost of producing one more unit or a few more units of output. The marginal cost for one additional unit produced is either 5 for any unit except the 101 st 201 st etc. If the cost of the first widget is.

A the change in total quantity that results from a one-unit increase in the price of the good. 2 Constant marginal costs occur when production of each individual unit costs. Thus the marginal cost for each of those marginal 20 units will be 8020 or 4 per haircut.

In this example marginal costs for various activities exist. A constant cost industry is an industry where each firms costs arent impacted by the entry or exit of new firms. B more than the previous one.

A less than the previous one. In this situation increasing production volume causes marginal costs to go down. What is the monopolists profit-maximizing.

B more than the previous one to produce. E it will always make zero economic profit. Setting MR equal to MC to determine the profit-maximizing quantity.

Highest of all the individual firms marginal cost curves b. Pages 180 Ratings 92 66 61 out of 66 people found this document helpful. D nothing to produce.

The following table gives the firms short run production function. More formally it is the derivative of the total cost function with respect to output. Public Choice 172 1 45-73.

This is the idea behind warehouse stores like Costco or Walmart. A less than the previous one. The total cost per hat would then drop to 175 1 fixed cost per unit 075 variable costs.

Marginal costs are important because economic decisions are made at the margin. P 27 15567 185. Less than the marginal cost an activity should be reduced.

Constant marginal costs occur when production of each individual unit costs. Constant marginal costs occur when each individual unit costs A less than the previous one to produce. Marginal cost is a constant 10.

The monopolists maximizing output occurs where marginal revenue equals marginal cost. Where the marginal costs would be 1005. 6Q Marginal cost of production is constant and equal to 20 and there are no fixed costs.

Efficient collective decision-making marginal cost pricing and quadratic voting. Suppose a competitive firm can sell its output for 11 per unit. To find the profit-maximizing price substitute this quantity into the demand equation.

For example as quantity produced increases from 40 to 60 haircuts total costs rise by 400 320 or 80. When a decision maker makes a quick decision without taking the time to compare the opportunity cost of all possible options he is using. 61Constant marginal costs occur when production of each individual unit costs.

Marginal cost is the increment in cost that occurs when the output produced is increased by one unit. C economic profit divided by the quantity sold. Mathematically marginal cost is the change in total cost divided by the change in output.

The firm will maximize profit with. The firm has total fixed costs of 9 and a constant marginal cost of 3 per unit. Constant marginal costs occur when each individual unit costs.

The marginal cost of introducing a new product line would be 10000. Table 7 outlines three examples of how the total cost will change with each production technology as the cost of labor changes. Servicing one additional customer would cost 2000.

More than the previous one. School Baruch College CUNY. A larger factory can produce at a lower average cost than a smaller factory.

The same to produce as the previous one. When will a firm find the optimal level of. The same as the previous one.

Constant marginal costs occur when each individual unit costs A. The same to produce as the previous one. Less than the previous one.

Suppose all firms have constant marginal costs that. Suppose all firms have constant marginal costs that are the same for each firm. Thus the marginal cost for each of those marginal 20.

27 - 3Q 10 or Q 567. Workers cost 40 machines cost 80. As the cost of labor rises from example A to B to C the firm will choose to substitute away from labor and use more machinery.

If average cost is the cost of the average unit of output produced marginal cost is the cost of each individual unit produced. C the same to produce as the previous one. Economies of scale refers to the situation where as the quantity of output goes up the cost per unit goes down.

D the change in economic profit that. Less than the previous one to produce. B more than the previous one.

More than the previous one to produce. We calculate marginal cost by taking the change in total cost and dividing it by the change in quantity. 8 Marginal revenue is.

C the same as the previous oneD more than the next one. For example as quantity produced increases from 40 to 60 haircuts total costs rise by 400 320 or 80. More than the next one.

B the change in total revenue that results from a one-unit increase in the quantity sold. For example the economic decision of a physician practice to expand or reduce a particular service in response. Learn about the difference between the short run market supply curve and the long run market supply curve for perfectly competitive firms in constant cost industries in this video.

Course Title ECON 3100.

/MinimumEfficientScaleMES2-c9372fffba0a4a1ab4ab0175600afdb6.png)

Minimum Efficient Scale Mes Definition

Diagrams Of Cost Curves Economics Help

Micro Chapter 8 Perfect Competition Flashcards Quizlet

Comments

Post a Comment